The Quantum Leap: Renko + ML(Note: This indicator uses the BackQuant & SuperTrend which takes a 4-5 seconds to load)

This strategy uses the following indicators (please see source code)

Synthetic Renko: Ignores time and focuses purely on price movement to detect clear trend reversals (Red-to-Green).

ATR (Average True Range): Measures volatility to calculate the Renko brick sizes and SuperTrend sensitivity.

Adaptive SuperTrend: A trend filter that uses volatility clustering to confirm if the market is currently in a "Bearish" state.

RSI (Relative Strength Index): A momentum gauge ensuring the asset is "Oversold" (exhausted) before we consider a setup.

Monthly Pivots: Horizontal support lines based on last month's data acting as price "floors" (S1, S2, S3).

SMA (Simple Moving Average): A 100-bar average ensuring we are strictly buying below the long-term mean (deep value).

BackQuant (KNN): A Machine Learning engine that compares current data to historical patterns to predict immediate momentum.

This is a sophisticated, multi-stage strategy script. It combines "Old School" price action (Renko) with "New School" Machine Learning (KNN and Clustering).

Here is the high-level summary of how we will break this down:

Topic 1: The "Bottom Hunter" Setup. How the script uses Renko bricks and aggressive filtering (SuperTrend, SMA, RSI, Pivots) to find a potential market bottom.

Topic 2: The ML Engine (BackQuant & SuperTrend). How the script uses K-Nearest Neighbors (KNN) to predict momentum and Volatility Clustering to adjust the SuperTrend.

Topic 3: The "Leap" Execution. How the script synchronizes the Setup (Topic 1) with the ML Trigger (Topic 2) using a time window.

Topic 1: The "Bottom Hunter" Setup

This script is designed as a Mean Reversion strategy (often called "catching a falling knife" or "bottom fishing"). It is trying to find the exact moment a downtrend stops and reverses.

Most strategies buy when price is above the 200 SMA or above the SuperTrend. This script does the exact opposite.

The Logic:

Renko Bricks: It simulates Renko bricks internally (without changing your chart view). It waits for a specific pattern: A Red Brick followed immediately by a Green Brick (a reversal).

The "Bearish" Filters: To generate a "WATCH" signal, the following must be true:

Price < SuperTrend: The market must officially be in a downtrend.

Price < SMA: Long-term trend is down.

Price < Monthly Pivot: Price is deeply discounted.

RSI < Threshold: The asset is oversold (exhausted).

Recommended Settings for daily signals for Stocks :

Confirmation : 10. (How many bars after Renko Buy signal the AI has to identify a bullish move).

Percentage : 2 (This is the Renko bar size. This represents 2% move.)

SMA: 100 (Signal must be found below 100 SMA)

Price must be below: PIVOT (This is the monthly Pivot levels)

Cerca negli script per "the script"

Regime [CHE] Regime — Minimal HTF MACD histogram regime marker with a simple rising versus falling state.

Summary

Regime is a lightweight overlay that turns a higher-timeframe-style MACD histogram condition into a simple regime marker on your chart. It queries an imported core module to determine whether the histogram is rising and then paints a consistent marker color based on that boolean state. The output is intentionally minimal: no lines, no panels, no extra smoothing visuals, just a repeated marker that reflects the current regime. This makes it useful as a quick context filter for other signals rather than a standalone system.

Motivation: Why this design?

A common problem in discretionary and systematic workflows is clutter and over-interpretation. Many regime tools draw multiple plots, which can distract from price structure. This script reduces the regime idea to one stable question: is the MACD histogram rising under a given preset and smoothing length. The core logic is delegated to a shared module to keep the indicator thin and consistent across scripts that rely on the same definition.

What’s different vs. standard approaches?

Reference baseline: A standard MACD histogram plotted in a separate pane with manual interpretation.

Architecture differences:

Uses a shared library call for the regime decision, rather than re-implementing MACD logic locally.

Uses a single boolean output to drive marker color, rather than plotting histogram bars.

Uses fixed marker placement at the bottom of the chart for consistent visibility.

Practical effect:

You get a persistent “context layer” on price without dedicating a separate pane or reading histogram amplitude. The chart shows state, not magnitude.

How it works (technical)

1. The script imports `chervolino/CoreMACDHTF/2` and calls `core.is_hist_rising()` on each bar.

2. Inputs provide the source series, a preset string for MACD-style parameters, and a smoothing length used by the library function.

3. The library returns a boolean `rising` that represents whether the histogram is rising according to the library’s internal definition.

4. The script maps that boolean to a color: yellow when rising, blue otherwise.

5. A circle marker is plotted on every bar at the bottom of the chart, colored by the current regime state. Only the most recent five hundred bars are displayed to limit visual load.

Notes:

The exact internal calculation details of `core.is_hist_rising()` are not shown in this code. Any higher timeframe mechanics, security usage, or confirmation behavior are determined by the imported library. (Unknown)

Parameter Guide

Source — Selects the price series used by the library call — Default: close — Tips: Use close for consistency; alternate sources may shift regime changes.

Preset — Chooses parameter preset for the library’s MACD-style configuration — Default: 3,10,16 — Trade-offs: Faster presets tend to flip more often; slower presets tend to react later.

Smoothing Length — Controls smoothing used inside the library regime decision — Default: 21 — Bounds: minimum one — Trade-offs: Higher values typically reduce noise but can delay transitions. (Library behavior: Unknown)

Reading & Interpretation

Yellow markers indicate the library considers the histogram to be rising at that bar.

Blue markers indicate the library considers it not rising, which may include falling or flat conditions depending on the library definition. (Unknown)

Because markers repeat on every bar, focus on transitions from one color to the other as regime changes.

This tool is best read as context: it does not express strength, only direction of change as defined by the library.

Practical Workflows & Combinations

Trend following:

Use yellow as a condition to allow long-side entries and blue as a condition to allow short-side entries, then trigger entries with your primary setup such as structure breaks or pullback patterns. (Optional)

Exits and stops:

Consider tightening management after a color transition against your position direction, but do not treat a single flip as an exit signal without price-based confirmation. (Optional)

Multi-asset and multi-timeframe:

Keep `Source` consistent across assets.

Use the slower preset when instruments are noisy, and the faster preset when you need earlier context shifts. The best transferability depends on the imported library’s behavior. (Unknown)

Behavior, Constraints & Performance

Repaint and confirmation:

This script itself uses no forward-looking indexing and no explicit closed-bar gating. It evaluates on every bar update.

Any repaint or confirmation behavior may come from the imported library. If the library uses higher timeframe data, intrabar updates can change the state until the higher timeframe bar closes. (Unknown)

security and HTF:

Not visible here. The library name suggests HTF behavior, but the implementation is not shown. Treat this as potentially higher-timeframe-driven unless you confirm the library source. (Unknown)

Resources:

No loops, no arrays, no heavy objects. The plotting is one marker series with a five hundred bar display window.

Known limits:

This indicator does not convey histogram magnitude, divergence, or volatility context.

A binary regime can flip in choppy phases depending on preset and smoothing.

Sensible Defaults & Quick Tuning

Starting point:

Source: close

Preset: 3,10,16

Smoothing Length: 21

Tuning recipes:

Too many flips: choose the slower preset and increase smoothing length.

Too sluggish: choose the faster preset and reduce smoothing length.

Regime changes feel misaligned with your entries: keep the preset, switch the source back to close, and tune smoothing length in small steps.

What this indicator is—and isn’t

This is a minimal regime visualization and a context filter. It is not a complete trading system, not a risk model, and not a prediction engine. Use it together with price structure, execution rules, and position management. The regime definition depends on the imported library, so validate it against your market and timeframe before relying on it.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

MACD HTF Hardcoded

Dobrusky Pressure CoreWhat it does & who it’s for

Dobrusky Pressure Core is a volume by time replacement for traders who care about which side actually controls each bar. Instead of just plotting total volume, it splits each bar into estimated buy vs sell pressure and overlays a custom, session-aware volume baseline. It’s built for discretionary traders who want more nuanced volume context for entries, breakouts, and pullbacks.

Core ideas

Buy/sell pressure split: Each bar’s volume is broken into estimated buying and selling pressure.

Dominant side highlighting: The dominant side (buy or sell) is always displayed starting from the bottom of the bar, so you can quickly see who “owned” that bar.

Median-based baseline: Uses the median of the last N bars (50 by default) to build a robust volume baseline that’s less sensitive to one-off spikes.

Session-aware behavior: Baseline is calculated from Regular Trading Hours (RTH) by default, with an option to include Extended Hours (ETH) and a control to force Regular data on higher timeframes.

Volume regimes: Three multipliers (1x, 1.5x, 2x by default) show normal, high, and extreme volume regions.

Flexible display: Baseline can be shown as lines or as columns behind the volume, with full color customization.

How the pressure logic works

For each bar, the script:

Adjusts the range for gaps relative to the prior close so the “true” traded range is more consistent.

Computes buy pressure as a proportion of the adjusted range from low to close.

Defines sell pressure as: total volume minus buy pressure.

Marks the bar as buy-dominant if buy pressure ≥ sell pressure, otherwise sell-dominant, and colors the dominant side from the bottom to at least the midpoint using the selected buy/sell colors.

In practice, this turns basic volume columns into bars where the internal split and dominant side are clearly visible, helping you judge whether aggressive buyers or sellers truly controlled the bar instead of just looking at the price action.

Volume baseline & session logic

The script builds a session-aware baseline from recent volume:

Baseline length: A rolling window (default 50 bars) is used to compute a median volume value instead of a simple moving average.

RTH-only by default: By default, the baseline is built from Regular Trading Hours bars only. During extended hours, the baseline effectively “freezes” at the last RTH-derived value unless you choose to include extended session data.

Extended mode: If you select Extended mode, the script builds separate rolling baselines for RTH and ETH trading, using the appropriate one depending on the current session.

Force Regular Above Timeframe: On timeframes equal to or higher than your chosen threshold, the baseline automatically uses Regular session data, even if Extended is selected.

Multipliers: Three adjustable multipliers (1x, 1.5x, 2x by default) create normal, high, and extreme volume bands for quick identification.

This lets you choose whether you want a pure RTH reference or a baseline that adapts to extended-session activity.

Example ways to use it

1. Replace standard volume bars

Add Dobrusky Pressure Core to your volume pane and hide the default volume if you prefer a clean look.

Use the colors and split to see at a glance whether buyers or sellers were dominant on each bar.

2. Pressure confirmation for entries

For longs (example concept; adapt to your own rules):

Require that the entry bar’s buy pressure is greater than the previous bar’s sell pressure , or

If the entry and prior bar are both buy-dominant, require that the entry bar has more buy pressure than the prior bar.

This helps avoid taking a long when buying pressure is clearly fading relative to what sellers recently showed. A mirrored idea can be used for short setups with sell pressure.

3. Context from baseline multipliers

Use ~1x baseline as “normal” volume.

Watch for bars at or above 1.5x baseline when you want to see increased participation.

Treat 2x baseline and above as “extreme” volume zones that may mark climactic or especially important bars.

In practice, the baseline and multipliers are best used as context and filters, not as rigid rules.

Settings overview

Display

- Show Volume Baseline: toggle the baseline and its levels on or off.

- Baseline Display: choose between Line or Bars for the baseline visualization.

Baseline Calculation

- Length: lookback for the median baseline (default 50, configurable).

- Baseline Session Data: choose Regular or Extended to control which session data feeds the baseline.

Session Controls

- Regular Session (Local to TZ): define your RTH window (e.g., 0930-1600).

- Session Time Zone: choose the time zone used for that window.

- Force Regular Above Timeframe: on higher timeframes, force the baseline to use Regular session data only.

Baseline Levels

- Show Level x Multiplier 1/2/3: toggle each volume regime level.

- Multiplier 1/2/3: define what you consider normal, high, and extreme volume (defaults: 1.0, 1.5, 2.0).

Colors

- Buy Volume / Sell Volume: choose colors for buy and sell pressure.

- Baseline Bars (Base / x2 / x3): colors when the baseline is drawn as columns.

- Baseline Line (Base / x2 / x3): colors when the baseline is drawn as lines.

Limitations & best practices

This is a decision-support and visualization tool, not a buy/sell signal generator.

Best suited to markets where volume data is meaningful (e.g., index futures, liquid equities, liquid crypto).

The usefulness of any volume-based metric depends on the underlying data feed and instrument structure.

Always combine pressure and baseline context with your own strategy, risk management, and testing.

Originality

Most volume tools either show total volume only or compare it to a simple moving average. Dobrusky Pressure Core combines:

An intrabar buy/sell pressure split based on a gap-adjusted price range.

A median-based, configurable baseline built from session-specific data.

Session-aware behavior that keeps the baseline focused on Regular hours by default, with the option to incorporate Extended hours and force Regular data on higher timeframes.

The goal is to give traders a richer, session-aware view of participation and pressure that standard volume bars and simple SMA overlays don’t provide, while keeping everything transparent and open-source so users can review and adapt the logic.

PM Range Breaker [CHE] PM Range Breaker — Premarket bias with first-five range breaks, optional SWDEMA regime latch, and simple two-times-range targets

Summary

This indicator sets a once-per-day directional bias during New York premarket and then tracks a strict first-five-minutes range from the session open. After the first five complete, it marks clean breakouts and can project targets at two times the measured range. A second mode latches an EMA-based regime to inform the bias and optional background tinting. A compact panel reports live state, first-five levels, and rolling hit rates of both bias modes using a user-defined midday close for statistics.

Motivation: Why this design?

Intraday traders often get whipsawed by early noise or by fast flips in trend filters. This script commits to a bias at a single premarket minute and then waits for the market to present an objective structure: the first-five range. Breaks after that window are clearer and easier to manage. The alternative SWDEMA regime gives a slower, latched context for users who prefer a trend scaffold rather than a midpoint reference.

What’s different vs. standard approaches?

Baseline: Typical open-range-breakout lines or a single moving-average filter without daily commitment.

Architecture differences:

Bias decision at a fixed New York time using either a midpoint lookback (“Classic”) or a two-EMA regime latch (“SWDEMA”).

Strict five-minute window from session open; breakout shapes print only after that window.

Single-shot breakout direction per session (debounce) and optional two-times-range targets.

On-chart panel with hit rates using a configurable midday close for statistics.

Practical effect: Cleaner visuals, fewer repeated signals, and a traceable daily decision that can be evaluated over time.

How it works (technical)

Time handling uses New York session times for premarket decision, open, first-five end, and a midday statistics checkpoint.

Classic bias: A midpoint is computed from the highest and lowest over a user period; at the premarket minute, the bias is set long when the close is above the midpoint, short otherwise.

SWDEMA bias: Two EMAs define a regime score that requires price and trend agreement; when both agree on a confirmed bar, the regime latches. At the premarket minute, the daily bias is set from the current regime.

The first-five range captures high and low from open until the end minute, then freezes. Breakouts are detected after that window using close-based cross logic.

The script draws range lines and optional targets at two times the frozen range. A session break direction latch prevents duplicate break markers.

Statistics compare daily open and a configurable midday close to record if the chosen bias aligned with the move.

Optional elements include EMA lines, midpoint line, latched-regime background, and regime switch markers.

Data aggregation for day logic and the first-five window is sampled on one-minute data with explicit lookahead off. On charts above one minute, values update intra-bar until the underlying minute closes.

Parameter Guide

Premarket Start (NY) — Minute when the bias is decided — Default: 08:30 — Move earlier for more stability; later for recency.

Market Open (NY) — Session start used for the first-five window — Default: 09:30 — Align to instrument’s RTH if different.

First-5 End (NY) — End of the first-five window — Default: 09:35 — Extend slightly to capture wider opening ranges.

Day End (NY) for Stats — Midday checkpoint for hit rate — Default: 12:00 — Use a later time for a longer evaluation window.

Show First-5 Lines — Draw the frozen range lines — Default: On — Turn off if your chart is crowded.

Show Bias Background (Session) — Tint by daily bias during session — Default: On — Useful for directional context.

Show Break Shapes — Print breakout triangles — Default: On — Disable if you only want lines and alerts.

Show 2R Targets (Optional) — Plot targets at two times the range — Default: On — Switch off if you manage exits differently.

Line Length Right — Extension length of drawn lines — Default: 20 (bars) — Increase for slower timeframes.

High/Low Line Colors — Visual colors for range levels — Defaults: Green/Red — Adjust to your theme.

Long/Short Bias Colors — Background tints — Defaults: Green/Red with high transparency — Lower transparency for stronger emphasis.

Show Corner Panel — Enable the info panel — Default: On — Centralizes status and numbers.

Show Hit Rates in Panel — Include success rates — Default: On — Turn off to reduce panel rows.

Panel Position — Anchor on chart — Default: Top right — Move to avoid overlap.

Panel Size — Text size in panel — Default: Small — Increase on high-resolution displays.

Dark Panel — Dark theme for the panel — Default: On — Match your chart background.

Show EMA Lines — Plot blue and red EMAs — Default: Off — Enable for SWDEMA context.

Show Midpoint Line — Plot the midpoint — Default: Off — Useful for Classic mode visualization.

Midpoint Lookback Period — Bars for high-low midpoint — Default: 300 — Larger values stabilize; smaller values respond faster.

Midpoint Line Color — Color for midpoint — Default: Gray — A neutral line works best.

SWDEMA Lengths (Blue/Red) — Periods for the two EMAs — Defaults: 144 and 312 — Longer values reduce flips.

Sources (Blue/Red) — Price sources — Defaults: Close and HLC3 — Adjust if you prefer consistency.

Offsets (Blue/Red) — Pixel offsets for EMA plots — Defaults: zero — Use only for visual shift.

Show Latched Regime Background — Background by SWDEMA regime — Default: Off — Separate from session bias.

Latched Background Transparency — Opacity of regime background — Default: eighty-eight — Lower value for stronger tint.

Show Latch Switch Markers — Plot regime change markers — Default: Off — For auditing regime changes.

Bias Mode — Classic midpoint or SWDEMA latch — Default: Classic — Choose per your style.

Background Mode — Session bias or SWDEMA regime — Default: Session — Decide which background narrative you want.

Reading & Interpretation

Panel: Shows the active bias, first-five high and low, and a state that reads Building during the window, Ready once frozen, and Break arrows when a breakout occurs. Hit rates show the percentage of days where each bias mode aligned with the midday move.

Colors and shapes: Green background implies long bias; red implies short bias. Triangle markers denote the first valid breakout after the first-five window. Optional regime markers flag regime changes.

Lines: First-five high and low form the core structure. Optional targets mark a level at two times the frozen range from the breakout side.

Practical Workflows & Combinations

Trend following: Choose a bias mode. Wait for the first clean breakout after the first-five window in the direction of the bias. Confirm with structure such as higher highs and higher lows or lower highs and lower lows.

Exits and risk: Conservative users can trail behind the opposite side of the first-five range. Aggressive users can scale near the two-times-range target.

Multi-asset and multi-TF: Works well on intraday timeframes from one minute upward. For non-US sessions, adjust the time inputs to the instrument’s regular trading hours.

Behavior, Constraints & Performance

Repaint and confirmation: Bias and regime decisions use confirmed bars. Breakout signals evaluate on bar close at the chart timeframe. On higher timeframes, minute-based sources update within the live bar until the minute closes.

security and HTF: The script samples one-minute data. Lookahead is off. Values stabilize once the source minute closes.

Resources: `max_bars_back` is five thousand. Drawing objects and the panel update efficiently, with position extensions handled on the last bar.

Known limits: Midday statistics use the configured time, not the official daily close. Session logic assumes New York session timing. Targets are simple multiples of the first-five range and do not adapt to volatility beyond that structure.

Sensible Defaults & Quick Tuning

Start with Classic bias, midpoint lookback at three hundred, and all visuals on.

Too many flips in context → switch to SWDEMA mode or increase EMA lengths.

Breakouts feel noisy → extend the first-five end by a minute or two, or wait for a retest by your own rules.

Too sluggish → reduce midpoint lookback or shorten EMA lengths.

Chart cluttered → hide EMA or midpoint lines and keep only range levels and breakout shapes.

What this indicator is—and isn’t

This is a visualization and signal layer for session bias and first-five structure. It does not manage orders, position sizing, or risk. It is not predictive. Use it alongside market structure, execution rules, and independent risk controls.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

Many thanks to LonesomeTheBlue

for the original work. I adapted the midpoint calculation for this script. www.tradingview.com

ai quant oculusAI QUANT OCULUS

Version 1.0 | Pine Script v6

Purpose & Innovation

AI QUANT OCULUS integrates four distinct technical concepts—exponential trend filtering, adaptive smoothing, momentum oscillation, and Gaussian smoothing—into a single, cohesive system that delivers clear, objective buy and sell signals along with automatically plotted stop-loss and three profit-target levels. This mash-up goes beyond a simple EMA crossover or standalone TRIX oscillator by requiring confluence across trend, adaptive moving averages, momentum direction, and smoothed price action, reducing false triggers and focusing on high‐probability turning points.

How It Works & Why Its Components Matter

Trend Filter: EMA vs. Adaptive MA

EMA (20) measures the prevailing trend with fixed sensitivity.

Adaptive MA (also EMA-based, length 10) approximates a faster-responding moving average, standing in for a KAMA-style filter.

Bullish bias requires AMA > EMA; bearish bias requires AMA < EMA. This ensures signals align with both the underlying trend and a more nimble view of recent price action.

Momentum Confirmation: TRIX

Calculates a triple-smoothed EMA of price over TRIX Length (15), then converts it to a percentage rate-of-change oscillator.

Positive TRIX reinforces bullish entries; negative TRIX reinforces bearish entries. Using TRIX helps filter whipsaws by focusing on sustained momentum shifts.

Gaussian Price Smoother

Applies two back-to-back 5-period EMAs to the price (“gaussian” smoothing) to remove short-term noise.

Price above the smoothed line confirms strength for longs; below confirms weakness for shorts. This layer avoids entries on erratic spikes.

Confluence Signals

Buy Signal (isBull) fires only when:

AMA > EMA (trend alignment)

TRIX > 0 (momentum support)

Close > Gaussian (price strength)

Sell Signal (isBear) fires under the inverse conditions.

Requiring all three conditions simultaneously sharply reduces false triggers common to single-indicator systems.

Automatic Risk & Reward Plotting

On each new buy or sell signal (edge detection via not isBull or not isBear ), the script:

Stores entryPrice at the signal bar’s close.

Draws a stop-loss line at entry minus ATR(14) × Stop Multiplier (1.5) by default.

Plots three profit-target lines at entry plus ATR × Target Multiplier (1×, 1.5×, and 2×).

All previous labels and lines are deleted on each new signal, keeping the chart uncluttered and focusing only on the current trade.

Inputs & Customization

Input Description Default

EMA Length Period for the main trend EMA 20

Adaptive MA Length Period for the faster adaptive EM A substitute 10

TRIX Length Period for the triple-smoothed momentum oscillator 15

Dominant Cycle Length (Reserved) 40

Stop Multiplier ATR multiple for stop-loss distance 1.5

Target Multiplier ATR multiple for first profit target 1.5

Show Buy/Sell Signals Toggle on-chart labels for entry signals On

How to Use

Apply to Chart: Best on 15 m–1 h timeframes for swing entries or 5 m for agile scalps.

Wait for Full Confluence:

Look for the AMA to cross above/below the EMA and verify TRIX and Gaussian conditions on the same bar.

A bright “LONG” or “SHORT” label marks your entry.

Manage the Trade:

Place your stop where the red or green SL line appears.

Scale or exit at the three yellow TP1/TP2/TP3 lines, automatically drawn by volatility.

Repeat Cleanly: Each new signal clears prior annotations, ensuring you only track the active setup.

Why This Script Stands Out

Multi-Layer Confluence: Trend, momentum, and noise-reduction must all align, addressing the weaknesses of single-indicator strategies.

Automated Trade Management: No manual plotting—stop and target lines appear seamlessly with each signal.

Transparent & Customizable: All logic is open, adjustable, and clearly documented, allowing traders to tweak lengths and multipliers to suit different instruments.

Disclaimer

No indicator guarantees profit. Always backtest AI QUANT OCULUS extensively, combine its signals with your own analysis and risk controls, and practice sound money management before trading live.

MTF Dashboard 9 Timeframes + Signals# MTF Dashboard Pro - Multi-Timeframe Confluence Analysis System

## WHAT THIS SCRIPT DOES

This script creates a comprehensive dashboard that simultaneously analyzes market conditions across 9 different timeframes (1m, 5m, 15m, 30m, 1H, 4H, Daily, Weekly, Monthly) using a proprietary confluence scoring methodology. Unlike simple multi-timeframe displays that show individual indicators separately, this script combines trend analysis, momentum, volatility signals, and volume analysis into unified confluence scores for each timeframe.

## WHY THIS COMBINATION IS ORIGINAL AND USEFUL

**The Problem Solved:** Most traders manually check multiple timeframes and struggle to quickly assess overall market bias when different timeframes show conflicting signals. Existing MTF scripts typically display individual indicators without synthesizing them into actionable intelligence.

**The Solution:** This script implements a mathematical confluence algorithm that:

- Weights each indicator's signal strength (trend direction, RSI momentum, MACD volatility, volume analysis)

- Calculates normalized scores across all active timeframes

- Determines overall market bias with statistical confidence levels

- Provides instant visual feedback through color-coded symbols and star ratings

**Unique Features:**

1. **Confluence Scoring Algorithm**: Mathematically combines multiple indicator signals into a single confidence rating per timeframe

2. **Market Bias Engine**: Automatically calculates overall directional bias with percentage strength across all selected timeframes

3. **Dynamic Display System**: Real-time updates with customizable layouts, color schemes, and selective timeframe activation

4. **Statistical Analysis**: Provides bullish/bearish vote counts and overall confluence percentages

## HOW THE SCRIPT WORKS TECHNICALLY

### Core Calculation Methodology:

**1. Trend Analysis (EMA-based):**

- Fast EMA (default: 9) vs Slow EMA (default: 21) crossover analysis

- Returns values: +1 (bullish), -1 (bearish), 0 (neutral)

**2. Momentum Analysis (RSI-based):**

- RSI levels: >70 (strong bullish +2), >50 (bullish +1), <30 (strong bearish -2), <50 (bearish -1)

- Provides overbought/oversold context for trend confirmation

**3. Volatility Analysis (MACD-based):**

- MACD line vs Signal line positioning

- Histogram strength comparison with previous bar

- Combined score considering both direction and momentum strength

**4. Volume Analysis:**

- Current volume vs 20-period moving average

- Thresholds: >150% MA (strong +2), >100% MA (bullish +1), <50% MA (weak -2)

**5. Confluence Calculation:**

```

Confluence Score = (Trend + RSI + MACD + Volume) / 4.0

```

**6. Market Bias Determination:**

- Counts bullish vs bearish signals across all active timeframes

- Calculates bias strength percentage: |Bullish Count - Bearish Count| / Total Active TFs * 100

- Determines overall market direction: BULLISH, BEARISH, or NEUTRAL

### Multi-Timeframe Implementation:

Uses `request.security()` calls to fetch data from each timeframe, ensuring all calculations are performed on the respective timeframe's data rather than current chart timeframe, providing accurate multi-timeframe analysis.

## HOW TO USE THIS SCRIPT

### Initial Setup:

1. **Timeframe Selection**: Enable/disable specific timeframes in "Timeframe Selection" group based on your trading style

2. **Indicator Configuration**: Adjust EMA periods (Fast: 9, Slow: 21), RSI length (14), and MACD settings (12/26/9) to match your analysis preferences

3. **Display Options**: Choose table position, text size, and color scheme for optimal visibility

### Reading the Dashboard:

**Symbol Interpretation:**

- ⬆⬆ = Strong bullish signal (score ≥ 2)

- ⬆ = Bullish signal (score > 0)

- ➡ = Neutral signal (score = 0)

- ⬇ = Bearish signal (score < 0)

- ⬇⬇ = Strong bearish signal (score ≤ -2)

**Confluence Stars:**

- ★★★★★ = Very high confidence (score > 0.75)

- ★★★★☆ = High confidence (score > 0.5)

- ★★★☆☆ = Medium confidence (score > 0.25)

- ★★☆☆☆ = Low confidence (score > 0)

- ★☆☆☆☆ = Very low confidence (score > -0.25)

**Market Bias Section:**

- Shows overall market direction across all active timeframes

- Strength percentage indicates conviction level

- Overall confluence score represents average agreement across timeframes

### Trading Applications:

**Entry Signals:**

- Look for high confluence (4-5 stars) across multiple timeframes in same direction

- Higher timeframe alignment provides stronger signal validation

- Use confluence percentage >75% for high-probability setups

**Risk Management:**

- Lower timeframe conflicts may indicate choppy conditions

- Neutral bias suggests ranging market - adjust position sizing

- Strong bias with high confluence supports larger position sizes

**Timeframe Harmony:**

- Short-term trades: Focus on 1m-1H alignment

- Swing trades: Emphasize 1H-Daily alignment

- Position trades: Prioritize Daily-Monthly confluence

## SCRIPT SETTINGS EXPLANATION

### Dashboard Settings:

- **Table Position**: Choose optimal location (Top Right recommended for most layouts)

- **Text Size**: Adjust based on screen resolution and preferences

- **Color Scheme**: Professional (default), Classic, Vibrant, or Dark themes

- **Background Color/Transparency**: Customize table appearance

### Timeframe Selection:

All timeframes optional - activate based on trading timeframe preference:

- **Lower Timeframes (1m-30m)**: Scalping and day trading

- **Medium Timeframes (1H-4H)**: Swing trading

- **Higher Timeframes (D-M)**: Position trading and long-term bias

### Indicator Parameters:

- **Fast EMA (Default: 9)**: Shorter period for trend sensitivity

- **Slow EMA (Default: 21)**: Longer period for trend confirmation

- **RSI Length (Default: 14)**: Standard momentum calculation period

- **MACD Settings (12/26/9)**: Standard MACD configuration for volatility analysis

### Alert Configuration:

- **Strong Signals**: Alerts when confluence >75% with clear directional bias

- **High Confluence**: Alerts when multiple timeframes strongly agree

- All alerts use `alert.freq_once_per_bar` to prevent spam

## VISUAL FEATURES

### Chart Elements:

- **Background Coloring**: Subtle background tint reflects overall market bias

- **Signal Labels**: Strong buy/sell labels appear on chart during high-confluence signals

- **Clean Presentation**: Dashboard overlays chart without interfering with price action

### Color Coding:

- **Green/Bullish**: Various green shades for positive signals

- **Red/Bearish**: Various red shades for negative signals

- **Gray/Neutral**: Neutral color for conflicting or weak signals

- **Transparency**: Configurable transparency maintains chart readability

## IMPORTANT USAGE NOTES

**Realistic Expectations:**

- This tool provides analysis framework, not trading signals

- Always combine with proper risk management

- Past performance does not guarantee future results

- Market conditions can change rapidly - use appropriate position sizing

**Best Practices:**

- Verify signals with additional analysis methods

- Consider fundamental factors affecting the instrument

- Use appropriate timeframes for your trading style

- Regular parameter optimization may be beneficial for different market conditions

**Limitations:**

- Effectiveness may vary across different instruments and market conditions

- Confluence scoring is mathematical model - not predictive guarantee

- Requires understanding of underlying indicators for optimal use

This script serves as a comprehensive analysis tool for traders who need quick, organized access to multi-timeframe market information with statistical confidence levels.

BARTRADINGPREDV4Please note, that all of the indicators on the chart are working together. I am showing all of the indicators so that you might see the benefits of these indicators working as one. Do your own research. Trade smart. I code tools not advice. So please make decisions based on your trading style and knowledge. Use my scripts freely but please note they are protected by Mozilla.

Script Summary: BARTRADINGPREDV4

This Pine Script indicator is a comprehensive trading tool that overlays on your TradingView chart. It combines moving averages, regression channels, volume analysis, RSI filtering, and pattern recognition to assist in making trading decisions. It also provides a forward-looking projection to help anticipate future price movement.

Key Features & Logic

1. Moving Averages

HMA (High Moving Average): Simple moving average of the high price over a user-defined lookback period.

LMA (Low Moving Average): Simple moving average of the low price over the same period.

HLMA (High-Low Moving Average): The average of HMA and LMA, providing a midline reference.

2. RSI Filtering

Optionally enables a Relative Strength Index (RSI) filter to help avoid trades when the market is not trending strongly.

Only allows buy signals if RSI is above 50, and sell signals if RSI is below 50 (if enabled).

3. Signal Generation

BUY Signal: Triggered when HL2 (average of OHLC) crosses over LMA and (optionally) RSI > 50.

SELL Signal: Triggered when HL2 crosses under HMA and (optionally) RSI < 50.

XSB (Extra Strong Buy): HL2 crosses over HMA, is above HLMA, up volume is greater than down volume, and (optionally) RSI > 50.

XBS (Extra Strong Sell): HL2 crosses under LMA, is below HLMA, down volume is greater than up volume, and (optionally) RSI < 50.

Enable/Disable XSB/XBS: You can turn these signals on or off via script inputs.

4. Take Profit (TP) and Stop Loss (SL) Levels

TP and SL are dynamically calculated based on the difference between HMA and LMA, providing contextually relevant exit levels.

5. Regression Channel and Prediction

Linear Regression Line: Plots a regression line over the lookback period to show the underlying trend.

ATR Channel: Adds an upper and lower channel around the regression line using ATR (Average True Range) for a realistic prediction envelope.

Forward Projection: Projects the regression line forward by a user-defined number of bars, visually showing where the trend could extend if current momentum persists.

6. Pattern Recognition

Higher Highs/Lows and Lower Highs/Lows: Marks bars where new higher highs/lows or lower highs/lows are set, helping you spot trend continuation or reversal points.

7. Status Table

A table shows the current price’s relationship to HMA, HLMA, and LMA, color-coded for quick visual interpretation.

User Instructions

Inputs

Number of Lookback Bars: Sets the period for all moving averages and regression calculations.

Prediction Length: (Legacy; not used in current logic.)

TURN ON OR OFF XSB/XBS Signal: Toggle extra strong buy/sell signals.

Enable RSI Filter: Only allow signals when RSI is in the correct zone.

RSI Period: Sets the sensitivity of the RSI filter.

Table Position: Choose where the status table appears on your chart.

ATR Length & Multiplier: Control the width of the regression prediction channel.

Bars Forward (Projection): Number of bars to project the regression line into the future.

How to Use

Add the script to your TradingView chart.

Adjust inputs to suit your asset and timeframe.

Interpret signals:

BUY (B) and SELL (S): Appear as green/red labels below/above bars.

XSB (blue) and XBS (orange): Indicate extra strong buy/sell conditions.

HH/HL (green triangles): New higher highs/lows.

LH/LL (red triangles): New lower highs/lows.

Watch the regression channel: The yellow regression line shows the trend; the shaded band indicates expected volatility.

Check the projection: The dashed magenta line projects the regression trend forward, giving a visual target for price continuation.

Use the table: Quickly see if price is above or below each moving average.

Interpreting the Prediction Aspects

Regression Line & Channel

Regression Line (Yellow): Represents the best-fit line of price over the lookback period, showing overall trend direction.

ATR Channel: The upper and lower bands (yellow, semi-transparent) account for typical volatility, suggesting a range where price is likely to stay if the trend continues.

Forward Projection

Dashed Magenta Line: Projects the regression line forward by the specified number of bars, using the current slope. This is a trend continuation forecast—not a guarantee, but a statistically reasonable path if current conditions persist.

How to use: If price is respecting the regression trend and within the channel, the projection provides a visual target for where price might go in the near future.

TP/SL Levels

TP (Take Profit): Suggests a price target above the current HL2, based on recent volatility.

SL (Stop Loss): Suggests a protective stop below HL2.

Best Practices & Warnings

No indicator is perfect! Always combine signals with your own analysis and risk management.

Regression projection is not a crystal ball: It simply extends the current trend, which can and will change, especially after big news or at support/resistance.

Use on liquid, trending assets for best results.

Adjust lookback and ATR settings for your market and timeframe.

Summary Table Example

Price vs HMA vs HLMA vs LMA

43000 +100 +50 -20

Green: Price is above average (bullish).

Red: Price is below average (bearish).

Yellow: Price is very close to the average (neutral).

Final Notes

This script is designed to be a multi-tool for trend trading and prediction, combining classic and modern techniques. The forward projection helps visualize possible future price action, while signals and overlays keep you informed of trend shifts and trade opportunities.

RSI Overbought/Oversold MTFRSI Overbought / Oversold MTF — Dashboard & Alerts

What it does

This script scans up to 13 symbols at once and shows their RSI readings on three lower‑time‑frames (1 min, 5 min, 15 min).

If all three RSIs for a symbol are simultaneously above the overbought threshold or below the oversold threshold, the script:

Prints the condition (“Overbought” / “Oversold”) in a color‑coded dashboard table.

Fires a one‑per‑bar alert so you never miss the move.

Key features

Feature Details

Multi‑symbol Default list includes BTC, ETH, SOL, BNB, XRP, ADA, AVAX, AVAAI, DOGE, VIRTUAL, SUI, ALCH, LAYER (all Binance pairs). Replace or reorder in the inputs.

Triple‑time‑frame check RSI is calculated on 1 m, 5 m, 15 m for each symbol.

Customizable thresholds Set your own RSI Period, Overbought and Oversold levels. Defaults: 14 / 70 / 30.

Color‑coded dashboard Top‑right table shows:

• Symbol name

• RSI 1 m / 5 m / 15 m (red = overbought, green = oversold, white = neutral)

• Overall Status column (“Overbought”, “Oversold”, “Mixed”).

Alerts built in Triggers once per bar whenever a symbol is overbought or oversold on all three time‑frames simultaneously.

Typical use cases

Scalp alignment — Enter when all short TFs agree on overbought/oversold extremes.

Mean‑reversion spotting — Identify stretched conditions across multiple coins without switching charts.

Quick sentiment scan — Glance at the dashboard to see where momentum is heating up or cooling down.

How to use

Add to chart (overlay = false; it sits in its own pane).

Adjust symbols & thresholds in the Settings panel.

Create alerts → choose “RSI Overbought/Oversold MTF” → “Any Alert() Function Call” to receive push, email, or webhook notifications.

Note: The script queries many symbols each bar; use on lower time‑frames only if your data limits allow.

For educational purposes only — not financial advice. Always test on paper before trading live.

High/Low mura visionDescription

High/Low mura vision plots static support and resistance lines based on the completed high and low values of the prior trading day, week and calendar month.

This script:

Anchors each level to the exact start and end bars of the completed period

Does not repaint or extend levels into the current period

Uses request.security() to retrieve only historical data (no lookahead)

This indicator was built to give traders clear, unambiguous reference points for breakout entries, pullback targets or confirmation of supply/demand zones without guessing where to draw manually.

How It Works

At the close of each daily candle, the script captures high and low via request.security() and draws flat lines spanning only that day’s bars.

Similarly, at the close of Friday’s weekly candle and the last bar of each calendar month, it draws the completed week’s and month’s high/low ranges.

All lines are deleted and redrawn only once per period completion, ensuring no forward painting or hidden repainting logic.

Key Features

No repaint: levels appear exactly once, immediately after the period closes

Period‑specific: lines confined to the bars of the prior day, week or month

Customizable: toggle each period on/off; choose independent colors, line styles (Solid, Dotted, Dashed) and width

Lightweight: minimal calculations for maximum performance on any timeframe

How to Use

Apply to any chart (M1 to MN).

In the Inputs panel, enable the levels you need: Yesterday, Last Week or Last Month.

Adjust High and Low line color, style and thickness to suit your chart layout.

Use these historic levels for support/resistance, breakout confirmation or confluence with other tools.

Inputs

Show Yesterday’s High: toggle yesterday’s high line

Show Yesterday’s Low: toggle yesterday’s low line

Show Last Week’s High: toggle last week’s high line

Show Last Week’s Low: toggle last week’s low line

Show Last Month’s High: toggle last month’s high line

Show Last Month’s Low: toggle last month’s low line

High Line Color / Low Line Color: choose colors for each set of lines

High Line Style / Low Line Style: select Solid, Dotted or Dashed

Line Width: adjust overall thickness

Disclaimer

This script is provided “as‐is” under the Public License. It is intended for educational and analytical purposes only and does not constitute trading or investment advice. Past performance does not guarantee future results. Always perform your own analysis and manage risk responsibly.

Bitcoin Power Law OscillatorThis is the oscillator version of the script. The main body of the script can be found here.

Understanding the Bitcoin Power Law Model

Also called the Long-Term Bitcoin Power Law Model. The Bitcoin Power Law model tries to capture and predict Bitcoin's price growth over time. It assumes that Bitcoin's price follows an exponential growth pattern, where the price increases over time according to a mathematical relationship.

By fitting a power law to historical data, the model creates a trend line that represents this growth. It then generates additional parallel lines (support and resistance lines) to show potential price boundaries, helping to visualize where Bitcoin’s price could move within certain ranges.

In simple terms, the model helps us understand Bitcoin's general growth trajectory and provides a framework to visualize how its price could behave over the long term.

The Bitcoin Power Law has the following function:

Power Law = 10^(a + b * log10(d))

Consisting of the following parameters:

a: Power Law Intercept (default: -17.668).

b: Power Law Slope (default: 5.926).

d: Number of days since a reference point(calculated by counting bars from the reference point with an offset).

Explanation of the a and b parameters:

Roughly explained, the optimal values for the a and b parameters are determined through a process of linear regression on a log-log scale (after applying a logarithmic transformation to both the x and y axes). On this log-log scale, the power law relationship becomes linear, making it possible to apply linear regression. The best fit for the regression is then evaluated using metrics like the R-squared value, residual error analysis, and visual inspection. This process can be quite complex and is beyond the scope of this post.

Applying vertical shifts to generate the other lines:

Once the initial power-law is created, additional lines are generated by applying a vertical shift. This shift is achieved by adding a specific number of days (or years in case of this script) to the d-parameter. This creates new lines perfectly parallel to the initial power law with an added vertical shift, maintaining the same slope and intercept.

In the case of this script, shifts are made by adding +365 days, +2 * 365 days, +3 * 365 days, +4 * 365 days, and +5 * 365 days, effectively introducing one to five years of shifts. This results in a total of six Power Law lines, as outlined below (From lowest to highest):

Base Power Law Line (no shift)

1-year shifted line

2-year shifted line

3-year shifted line

4-year shifted line

5-year shifted line

The six power law lines:

Bitcoin Power Law Oscillator

This publication also includes the oscillator version of the Bitcoin Power Law. This version applies a logarithmic transformation to the price, Base Power Law Line, and 5-year shifted line using the formula: log10(x) .

The log-transformed price is then normalized using min-max normalization relative to the log-transformed Base Power Law Line and 5-year shifted line with the formula:

normalized price = log(close) - log(Base Power Law Line) / log(5-year shifted line) - log(Base Power Law Line)

Finally, the normalized price was multiplied by 5 to map its value between 0 and 5, aligning with the shifted lines.

Interpretation of the Bitcoin Power Law Model:

The shifted Power Law lines provide a framework for predicting Bitcoin's future price movements based on historical trends. These lines are created by applying a vertical shift to the initial Power Law line, with each shifted line representing a future time frame (e.g., 1 year, 2 years, 3 years, etc.).

By analyzing these shifted lines, users can make predictions about minimum price levels at specific future dates. For example, the 5-year shifted line will act as the main support level for Bitcoin’s price in 5 years, meaning that Bitcoin’s price should not fall below this line, ensuring that Bitcoin will be valued at least at this level by that time. Similarly, the 2-year shifted line will serve as the support line for Bitcoin's price in 2 years, establishing that the price should not drop below this line within that time frame.

On the other hand, the 5-year shifted line also functions as an absolute resistance , meaning Bitcoin's price will not exceed this line prior to the 5-year mark. This provides a prediction that Bitcoin cannot reach certain price levels before a specific date. For example, the price of Bitcoin is unlikely to reach $100,000 before 2021, and it will not exceed this price before the 5-year shifted line becomes relevant. After 2028, however, the price is predicted to never fall below $100,000, thanks to the support established by the shifted lines.

In essence, the shifted Power Law lines offer a way to predict both the minimum price levels that Bitcoin will hit by certain dates and the earliest dates by which certain price points will be reached. These lines help frame Bitcoin's potential future price range, offering insight into long-term price behavior and providing a guide for investors and analysts. Lets examine some examples:

Example 1:

In Example 1 it can be seen that point A on the 5-year shifted line acts as major resistance . Also it can be seen that 5 years later this price level now corresponds to the Base Power Law Line and acts as a major support at point B(Note: Vertical yearly grid lines have been added for this purpose👍).

Example 2:

In Example 2, the price level at point C on the 3-year shifted line becomes a major support three years later at point D, now aligning with the Base Power Law Line.

Finally, let's explore some future price predictions, as this script provides projections on the weekly timeframe :

Example 3:

In Example 3, the Bitcoin Power Law indicates that Bitcoin's price cannot surpass approximately $808K before 2030 as can be seen at point E, while also ensuring it will be at least $224K by then (point F).

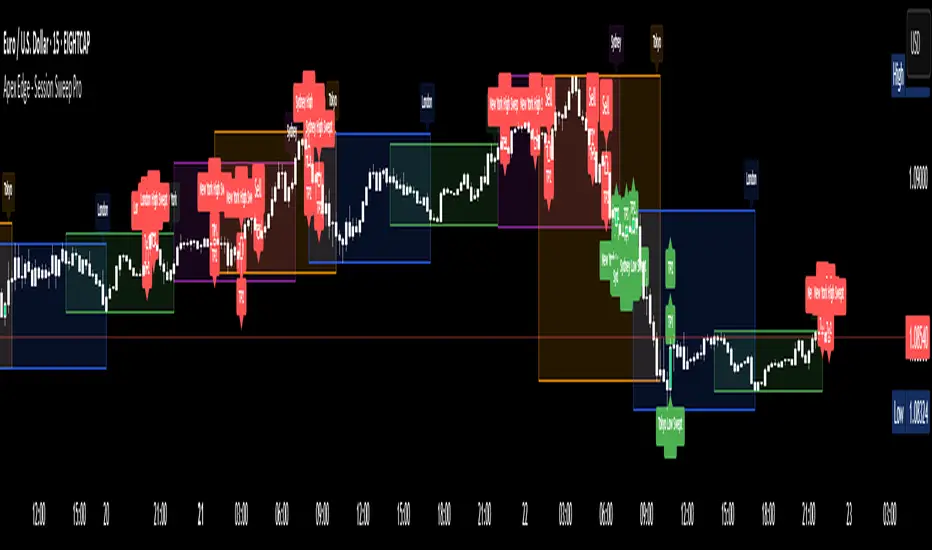

Apex Edge - Session Sweep ProApex Edge Session Sweep Pro

By Apex Edge | 2025 Edition

🔍 What is it?

The Apex Session Sweep Pro is a precision trading tool designed for identifying high-probability liquidity sweep entries during key global market sessions. It combines powerful sweep detection logic with dynamic candle colouring, session visualization, TP projections, and real-time alerts — all within a clean, performance-optimized Pine Script engine.

This is not your average session box indicator. This is Apex-grade.

⚙️ How it Works

The indicator detects session liquidity sweeps by tracking price action relative to previous session highs and lows. When a session high/low is swept (i.e., price breaches it and then closes in the opposite direction), it generates a signal:

Buy Signal → Price sweeps previous low and closes back above it

Sell Signal → Price sweeps previous high and closes back below it

Each session is boxed on the chart (Tokyo, London, New York, Sydney), color-coded, and dynamically labelled.

Upon detecting a valid sweep, the script:

Plots a small entry label (toggleable)

Projects up to 5 customizable TP levels

Coloured candles for visual trade direction

Alerts for Buy or Sell sweep signals (optional)

All elements are memory-managed and customizable to suit your trading style.

🧠 Key Features

✅ Smart Sweep Detection Logic

✅ Global Market Session Boxes (Custom Times)

✅ Toggleable Entry Labels + TP Levels

✅ Candle Colouring by Signal

✅ Manual TP input + TP toggles

✅ Real-time Alerts for Apex entries

🕒 Why Are My Sessions Offset?

Your chart’s time zone may be different from UTC. This script is UTC-based by design, so if your chart is set to UTC+1, for example, the sessions will appear one hour later. Either:

Adjust your chart to UTC or or Exchange for perfect alignment,

Or tweak the session input times manually.

🧰 Who is this for?

This tool is made for:

Intraday traders looking for sweeps into liquidity

SMC (Smart Money Concept) strategists

Forex, crypto, and indices traders

Anyone who uses session-based levels to define entries

Whether you scalp London or ride NY swings, this tool frames each session cleanly — and shows you where the traps are laid.

🚨 Disclaimer

This indicator is a technical tool, not financial advice. Use proper risk management. Past performance ≠ future results.

ICT Swiftedge# ICT SwiftEdge: Advanced Market Structure Trading System

**Overview**

ICT SwiftEdge is a powerful trading system built upon the foundation of ICTProTools' ICT Breakers, licensed under the Mozilla Public License 2.0 (mozilla.org). This script has been significantly enhanced by to combine market structure analysis with modern technical indicators and a sleek, AI-inspired statistics dashboard. The goal is to provide traders with a comprehensive tool for identifying high-probability trade setups, managing exits, and tracking performance in a visually intuitive way.

**Credits**

This script is a derivative work based on the original "ICT Breakers" by ICTProTools, used with permission under the Mozilla Public License 2.0. Significant enhancements, including RSI-MA signals, trend filtering, dynamic timeframe adjustments, dual exit strategies, and an AI-style statistics dashboard, were developed by . We express our gratitude to ICTProTools for their foundational work in market structure analysis.

**What It Does**

ICT SwiftEdge integrates multiple trading concepts to help traders identify and manage trades based on market structure and momentum:

- **Market Structure Analysis**: Identifies Break of Structure (BOS) and Market Structure Shift (MSS) patterns, which signal potential trend continuations or reversals. BOS indicates a continuation of the current trend, while MSS highlights a shift in market direction, providing key entry points.

- **RSI-MA Signals**: Generates "BUY" and "SELL" signals when BOS or MSS patterns align with the Relative Strength Index (RSI) smoothed by a Moving Average (RSI-MA). Signals are filtered to occur only when RSI-MA is above 50 (for buys) or below 50 (for sells), ensuring momentum supports the trade direction.

- **Trend Filtering**: Prevents multiple signals in the same trend, ensuring only one buy or sell signal per trend direction, reducing noise and improving trade clarity.

- **Dynamic Timeframe Adjustment**: Automatically adjusts pivot points, RSI, and MA parameters based on the selected chart timeframe (1M to 1D), optimizing performance across different market conditions.

- **Flexible Exit Strategies**: Offers two user-selectable exit methods:

- **Trailing Stop-Loss (TSL)**: Exits trades when price moves against the position by a user-defined distance (in points), locking in profits or limiting losses.

- **RSI-MA Exit**: Exits trades when RSI-MA crosses the 50 level, signaling a potential loss of momentum.

- Users can enable either or both strategies, providing flexibility to adapt to different trading styles.

- **AI-Style Statistics Dashboard**: Displays real-time trade performance metrics in a futuristic, neon-colored interface, including total trades, wins, losses, win/loss ratio, and win percentage. This helps traders evaluate the system's effectiveness without external tools.

**Why This Combination?**

The integration of these components creates a synergistic trading system:

- **BOS/MSS and RSI-MA**: Combining market structure breaks with RSI-MA ensures entries are based on both price action (structure) and momentum (RSI-MA), increasing the likelihood of high-probability trades.

- **Trend Filtering**: By limiting signals to one per trend, the system avoids overtrading and focuses on significant market moves.

- **Dynamic Adjustments**: Timeframe-specific parameters make the system versatile, suitable for scalping (1M, 5M) or swing trading (4H, 1D).

- **Dual Exit Strategies**: TSL protects profits during trending markets, while RSI-MA exits are ideal for range-bound or reversing markets, catering to diverse market conditions.

- **Statistics Dashboard**: Provides immediate feedback on trade performance, enabling data-driven decision-making without manual tracking.

This combination balances technical precision with user-friendly visuals, making it accessible to both novice and experienced traders.

**How to Use**

1. **Add to Chart**: Apply the script to any TradingView chart.

2. **Configure Settings**:

- **Chart Timeframe**: Select your chart's timeframe (1M to 1D) to optimize parameters.

- **Structure Timeframe**: Choose a timeframe for market structure analysis (leave blank for chart timeframe).

- **Exit Strategy**: Enable Trailing Stop-Loss (`useTslExit`), RSI-MA Exit (`useRsiMaExit`), or both. Adjust `tslPoints` for TSL distance.

- **Show Signals/Labels**: Toggle `showSignals` and `showExit` to display "BUY", "SELL", and "EXIT" labels.

- **Dashboard**: Enable `showDashboard` to view trade statistics. Customize colors with `dashboardBgColor` and `dashboardTextColor`.

3. **Trading**:

- Look for "BUY" or "SELL" labels to enter trades when BOS/MSS aligns with RSI-MA.

- Exit trades at "EXIT" labels based on your chosen strategy.

- Monitor the statistics dashboard to track performance (total trades, win/loss ratio, win percentage).

4. **Alerts**: Set up alerts for BOS, MSS, buy, sell, or exit signals using the provided alert conditions.

**License**

This script is licensed under the Mozilla Public License 2.0 (mozilla.org). The source code is available for review and modification under the terms of this license.

**Compliance with TradingView House Rules**

This publication adheres to TradingView's House Rules and Scripts Publication Rules. It provides a clear, self-contained description of the script's functionality, credits the original author (ICTProTools), and explains the rationale for combining indicators. The script contains no promotional content, offensive language, or proprietary restrictions beyond MPL 2.0.

**Note**

Trading involves risk, and past performance is not indicative of future results. Always backtest and validate the system on your preferred markets and timeframes before live trading.

Enjoy trading with ICT SwiftEdge, and let data-driven insights guide your decisions!

Liquidity Fracture DetectorThe Liquidity Fracture Detector is an advanced tool designed to identify micro-liquidity traps and structural fakeouts on intraday charts. These occur when the market appears to break out, only to quickly reverse — often triggered by stop hunts, inefficient fills, or manipulated order flow.

The script combines volume spikes, volatility anomalies, and price structure breaks to signal "fractures" — points where the market temporarily breaks its behavior, often followed by strong reversals or trend accelerations.

Detection logic in the script:

Volume spike greater than 2x the average (adjustable)

Volatility spike: candle range is > 1.5x the average

Extreme wicks: wick is larger than the candle body (a classic trap signal)

Structure break: price breaks previous high/low but closes back within the old range

Combine these elements → a “fracture” is marked

Visual representation:

Red background = potential bull trap (fake breakout to the upside)

Green background = potential bear trap (fake breakdown to the downside)

A label appears at each fracture: “Echo” with the number of previous hits

Ideal use cases:

Intraday trading (1m, 5m, 15m)

Crypto, indices, futures, and forex

Detecting reactive zones where the market takes a false direction

Confluence with S/R zones, order blocks, or liquidity pools

Fully customizable:

Volume and range sensitivity

Heatmap intensity

Toggle labels on/off

Note:

This script is intended to support discretionary analysis. It does not provide buy or sell signals and is not an automated strategy. Combine it with your own price action or order flow setup for optimal results.

Autofib Extensions | DTDHello trader comuunity!

I'm introducing another script that is part of my main day-trading strategy. We all know regardless of what strategy we use, we need to know what levels offer the least amount of risk to our trade entry and a great tool to anticipate how far a move might go or what level a move may retrace to are the Fibonacci Retracement and Extensions. This indicator combines both together, but with a twist.

The main elements of the script are:

1. Multiple Session High and Lows | Developing my first script led me to understand that measuring key times during each session provides understanding of the market's continuity. I have provided 3 "sessions' a user can define according to CST time where the script saves the high and low of that session window to produce the retracement and extensions from those plots. Currently, the levels are always plotted from low to high (with the 0 mark being the high) and negative values provided so the levels are consistent. You can toggle each session on or off.

2. Coloring Key Retracements / Extensions | I use a dark background for my charts so the default colors help me distinguish from other another indicator I use. Feel free to adjust the colors to your preference. I consider 3 different colors because of their significance. Retracements that you want to see continue fall back into the .50 to .618 level (this I consider the "Golden Zone"). While basic Elliott Wave Theory states a wave is completed near the 1.618 level (this I consider "Major Extensions"). Everything isn't noise, but minor levels in a larger sequence.

______________

Script Limitations

All of my scripts are made with the help of ChatGPT so there are going to be limitations. One current one that I have made progress on, but not fully is when you are viewing a timeframe where the candle doesn't start when a session window starts. On smaller timeframes like the 7-minute this is not an issue. However, on the hourly, if your session window starts at the half hour which the 3rd session default window does, the lines will not produce. I will hopefully have this rectified in the near future. I will open the script since none of this work is original in nature and I would love to see how others can create a better product. Also, this is mainly a futures trading tool. If you are using this on stocks you will find it not as useful if the session window is too wide since the script waits until the session window closes to calculate the extension values.

Cheers,

DTD

VNIndex Over 6.5% Downside Drop Indicator with TableOverview: The VNIndex 6.5% Downside Drop Indicator is a powerful tool designed to help traders and investors identify significant market drops on the VNIndex (or any other asset) based on a 6.5% downside threshold. This Pine Script® indicator automatically detects when the price of an asset drops by more than 6.5% within a single day, and visually marks those events on the chart.

Key Features:

6.5% Downside Drop Detection: Automatically calculates the daily percentage drop and identifies when the price falls by more than 6.5%.

Table Display: Displays the dates and corresponding percentage drops of all identified instances in a convenient table at the bottom right of the chart.

Markers: Red down-pointing markers are plotted above bars where the price drop exceeds the 6.5% threshold, making it easy to spot critical drop events at a glance.

Easy-to-Read Table: The table lists the date and drop percentage, updating dynamically as new drops are detected. This allows for easy tracking of significant downside moves over time.

How to Use:

Install the Script: Add this indicator to your TradingView chart.

Monitor Price Drops: The indicator will automatically detect when the price drops by over 6.5% from the previous close and display a marker on the chart and the table in the bottom right corner.

View the Table: The table displays the date and the percentage drop of each detected event, making it easy to track past significant moves.

Alerts: You can set an alert for 6.5% drops to receive notifications in real-time.

Customization Options:

The drop percentage threshold (6.5%) can be adjusted in the script to fit other market conditions or assets.

The table can be resized or styled based on user preference for better visibility.

Why Use This Indicator? This indicator is perfect for traders looking to spot large, significant price movements quickly. Large downside drops can signal potential market reversals or trading opportunities, and this tool helps you track such events effortlessly. Whether you're monitoring the VNIndex or any other asset, this indicator provides crucial insights into volatile price action, helping you make more informed decisions.

Open Source License: This indicator is open source and free to use under the Mozilla Public License 2.0. You are welcome to modify, distribute, and contribute to the project.

Contributions: Feel free to contribute improvements, fixes, or new features by creating a pull request. Let’s collaborate to make this indicator even better for the community!

Mogwai Method with RSI and EMA - BTCUSD 15mThis is a custom TradingView indicator designed for trading Bitcoin (BTCUSD) on a 15-minute timeframe. It’s based on the Mogwai Method—a mean-reversion strategy—enhanced with the Relative Strength Index (RSI) for momentum confirmation. The indicator generates buy and sell signals, visualized as green and red triangle arrows on the chart, to help identify potential entry and exit points in the volatile cryptocurrency market.

Components

Bollinger Bands (BB):

Purpose: Identifies overextended price movements, signaling potential reversions to the mean.

Parameters:

Length: 20 periods (standard for mean-reversion).

Multiplier: 2.2 (slightly wider than the default 2.0 to suit BTCUSD’s volatility).

Role:

Buy signal when price drops below the lower band (oversold).

Sell signal when price rises above the upper band (overbought).

Relative Strength Index (RSI):

Purpose: Confirms momentum to filter out false signals from Bollinger Bands.

Parameters:

Length: 14 periods (classic setting, effective for crypto).

Overbought Level: 70 (price may be overextended upward).

Oversold Level: 30 (price may be overextended downward).

Role:

Buy signal requires RSI < 30 (oversold).

Sell signal requires RSI > 70 (overbought).

Exponential Moving Averages (EMAs) (Plotted but not currently in signal logic):

Purpose: Provides trend context (included in the script for visualization, optional for signal filtering).

Parameters:

Fast EMA: 9 periods (short-term trend).

Slow EMA: 50 periods (longer-term trend).

Role: Can be re-added to filter signals (e.g., buy only when Fast EMA > Slow EMA).

Signals (Triangles):

Buy Signal: Green upward triangle below the bar when price is below the lower Bollinger Band and RSI is below 30.

Sell Signal: Red downward triangle above the bar when price is above the upper Bollinger Band and RSI is above 70.

How It Works

The indicator combines Bollinger Bands and RSI to spot mean-reversion opportunities:

Buy Condition: Price breaks below the lower Bollinger Band (indicating oversold conditions), and RSI confirms this with a reading below 30.

Sell Condition: Price breaks above the upper Bollinger Band (indicating overbought conditions), and RSI confirms this with a reading above 70.

The strategy assumes that extreme price movements in BTCUSD will often revert to the mean, especially in choppy or ranging markets.

Visual Elements

Green Upward Triangles: Appear below the candlestick to indicate a buy signal.

Red Downward Triangles: Appear above the candlestick to indicate a sell signal.

Bollinger Bands: Gray lines (upper, middle, lower) plotted for reference.

EMAs: Blue (Fast) and Orange (Slow) lines for trend visualization.

How to Use the Indicator

Setup

Open TradingView:

Log into TradingView and select a BTCUSD chart from a supported exchange (e.g., Binance, Coinbase, Bitfinex).

Set Timeframe:

Switch the chart to a 15-minute timeframe (15m).

Add the Indicator:

Open the Pine Editor (bottom panel in TradingView).

Copy and paste the script provided.

Click “Add to Chart” to apply it.

Verify Display:

You should see Bollinger Bands (gray), Fast EMA (blue), Slow EMA (orange), and buy/sell triangles when conditions are met.

Trading Guidelines

Buy Signal (Green Triangle Below Bar):

What It Means: Price is oversold, potentially ready to bounce back toward the Bollinger Band middle line.

Action:

Enter a long position (buy BTCUSD).

Set a take-profit near the middle Bollinger Band (bb_middle) or a resistance level.

Place a stop-loss 1-2% below the entry (or based on ATR, e.g., ta.atr(14) * 2).

Best Context: Works well in ranging markets; avoid during strong downtrends.

Sell Signal (Red Triangle Above Bar):

What It Means: Price is overbought, potentially ready to drop back toward the middle line.

Action:

Enter a short position (sell BTCUSD) or exit a long position.

Set a take-profit near the middle Bollinger Band or a support level.

Place a stop-loss 1-2% above the entry.

Best Context: Effective in ranging markets; avoid during strong uptrends.

Trend Filter (Optional):

To reduce false signals in trending markets, you can modify the script:

Add and ema_fast > ema_slow to the buy condition (only buy in uptrends).

Add and ema_fast < ema_slow to the sell condition (only sell in downtrends).

Check the Fast EMA (blue) vs. Slow EMA (orange) alignment visually.

Tips for BTCUSD on 15-Minute Charts

Volatility: BTCUSD can be erratic. If signals are too frequent, increase bb_mult (e.g., to 2.5) or adjust RSI levels (e.g., 75/25).

Confirmation: Use volume spikes or candlestick patterns (e.g., doji, engulfing) to confirm signals.

Time of Day: Mean-reversion works best during low-volume periods (e.g., Asian session in crypto).

Backtesting: Use TradingView’s Strategy Tester (convert to a strategy by adding entry/exit logic) to evaluate performance with historical BTCUSD data up to March 13, 2025.

Risk Management

Position Size: Risk no more than 1-2% of your account per trade.

Stop Losses: Always use stops to protect against BTCUSD’s sudden moves.

Avoid Overtrading: Wait for clear signals; don’t force trades in choppy or unclear conditions.

Example Scenario

Chart: BTCUSD, 15-minute timeframe.

Buy Signal: Price drops to $58,000, below the lower Bollinger Band, RSI at 28. A green triangle appears.

Action: Buy at $58,000, target $59,000 (middle BB), stop at $57,500.

Sell Signal: Price rises to $60,500, above the upper Bollinger Band, RSI at 72. A red triangle appears.

Action: Sell at $60,500, target $59,500 (middle BB), stop at $61,000.

This indicator is tailored for mean-reversion trading on BTCUSD. Let me know if you’d like to tweak it further (e.g., add filters, alerts, or alternative indicators)!

Wave Modulation Demo█ OVERVIEW